It's their secret plan to steal all your money. (Unfortunately, it will work.)

Boomers. Gen X. Millennial. Gen Z. It it's true, this will affect you.

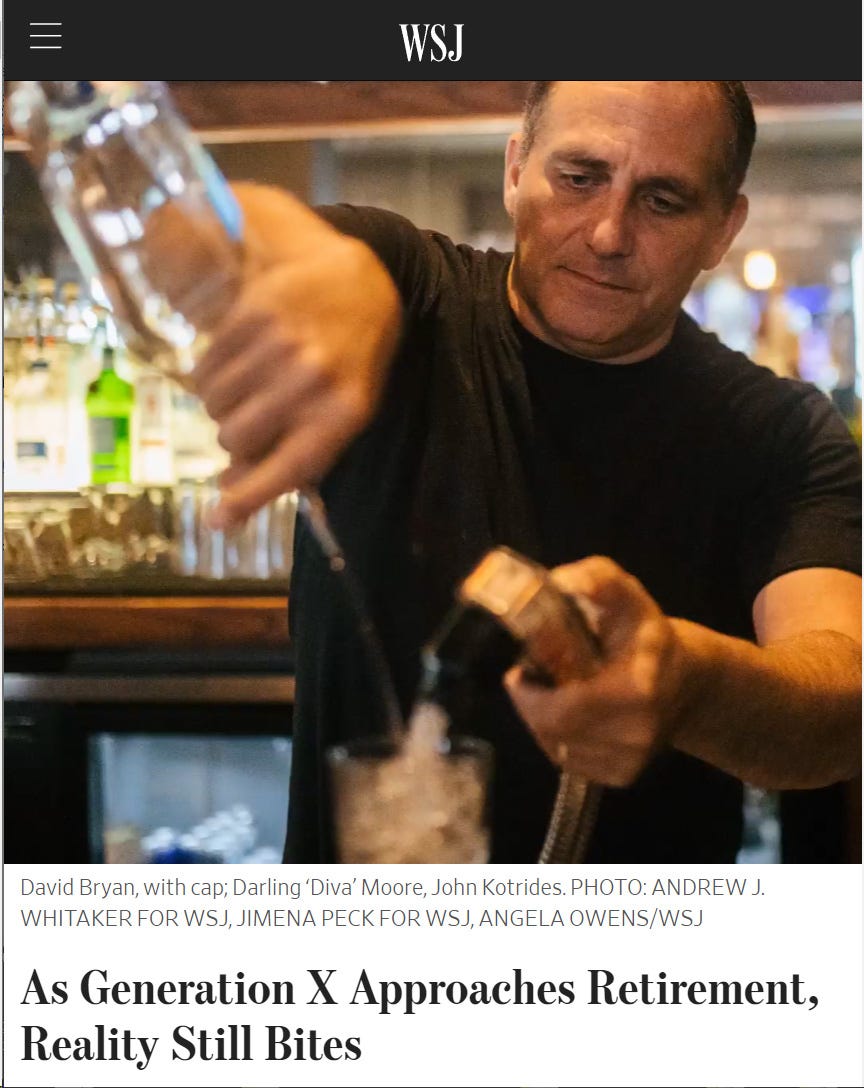

The oldest members of Gen X are turning 60 next year. Many can’t afford to stop working any time soon… “I fully expect to work until I die,” Nesbitt said. “It is what it is.”

Those are the first and last sentences of an article in the Wall Street Journal in August 2024 about how Generation X will not be able to afford to retire. But the reality is worse than the WSJ says. A lot worse. For one thing, the baby boomers probably won't be able to pay for the rest of their retirements either. There's a strong likelihood that the Boomers will die in poverty. Because of something no one seems to see coming.

If you are a Millennial or Gen Z, this story is about a disaster that will drastically affect you too. As we will show.

The Baby Boomers’ Retirement Money

Baby boomers have a lot of money, and they have a lot of it in the stock market. Boomers aged 55 and up control nearly 70% of U.S. household wealth, according to a 2024 survey by the St Louis Fed. The median in each of their 401(k)s and IRAs was about $160,000. And many boomers have retirement portfolios over and above the government 401(k)s and IRAs. Obviously the Boomers are at or nearing the age when they will need that money in those stock portfolios just to live. The boomers are counting on that money.

What happens if that money disappears? Soon? Because it probably will.

(If you already know all about how the Boomers and Gen X will probably lose their savings and go broke in droves, you might want to jump to “Conclusion: Why This is Important!”)

The Everything Bubble

For many years, experienced investors were interviewed on financial TV shows predicting a huge, long-lasting market crash, like the one in 1929. It had to happen, they said, because, fundamentally, the stock market was immensely overvalued. And it would take decades for the losses to be written off and for stocks to again reach their current prices. Because that is what happened in 1929.

Strange thing is, those old guys were fundamentally right. But that big, long crash never happened.

Why not?

Because the prognosticators didn't realize that the whole system had changed. And they no longer understood it. What they didn't understand was:

1. Big government bailouts

Crashes did indeed happen. But instead of the equities really being revalued at lower prices, the prices almost immediately went right back up, and soon became even more overvalued. That is because, starting with the Savings & Loan crash in 1980, a lot of rich people lost a lot of money, and instead of letting those people eat those losses, the government stepped in and bailed them out, at the expense of the rest of us.

It set a terrible precedent. The equities markets were, from the perspective of the government regulators, Too Big to Fail. When bubbles burst, they had to be reinflated by GoverFed.

2. The Buy-and-Hold Bubble

When it became clear that the government was not going to allow the Everything Bubble to burst, smart people learned to “buy the dip”. Because if you turned bearish, and sold or shorted the markets, you would lose. “You can't fight the Fed” because the feds will always step in and bail out the rich elites.

Baby Boomers and Gen X investors learned to ignore the dire predictions of sage, experienced investors who, as we said, predicted a huge, long-lasting market crash. Instead, the investors came to believe absolutely that buy-and-hold could not fail.

Now what?

You probably knew all that already. But you may not know what's likely to happen next. Nobody seems to be talking about it. Certainly not the leftist mass media or the politicians.

The fatal flaw of buy-and-hold: How the Baby Boomers forgot to sell their stocks.

Boomers and Gen X believe that buy-and-hold is a fundamental principle of investing in stocks. But in reality, that belief is an artifact of the government bailouts. However, even if the government did not step in and bail out rich people after crashes, buy-and-hold is only good for people in their youth and middle age. Because the truth of investing in growth equities (as opposed to investing for dividend income, which no one does anymore) is that you haven't really made any money until you sell.

In the era before government bailouts and too-big-to-fail, when investors got old they sold their growth stocks and bought equities that paid interest or dividends. But to investors born after World War II, buy-and-hold became written in stone. The first commandment. So the Boomers and Gen Xers bought and held. And held and held and held. As we will see.

The people investing for retirement no longer understood the truth that you haven't really made any money from investing in growth equities until you sell them. Until then, the value of your portfolio is just a number. And that number can fall to near zero, overnight. And if GoverFed does not bail out the markets after such a fall, then that low, low price can stay near zero for a long, long time.

Consider this: After the 1929 Crash, stocks lost nearly 90% of their value. And the Dow didn't fully recover until November 1954.

Because of buy-and-hold, corporations learned that you got stockholders not by paying dividends, but by showing growth. This means that if the market crashes, older investors are stuck holding shares that pay no dividends, or a percentage of dividends that is less than inflation. In other words, nothing.

The impoverishment of Americans over 55

Most Americans who have worked for a living plan to pay for their retirement by:

○ An IRA, 401K or other investment portfolio.

○ Social Security.

○ The equity in their homes.

If there is a big crash and the government doesn't bail out the market, those Americans will not be able to pay for retirement. A lot of boomers are depending upon their investment portfolios as we saw. They will be destitute.

○ If the investment in stocks lose 80% of their value, and the Government bailout doesn't arrive, then the stocks will not regain their value during the lifetimes of the investors. The Americans who own them will have to sell them at an 80% loss Just to pay living expenses.

○ “Social Security was never intended to be the sole source of income later in life,” Ramsey Alwin, CEO, National Council on Aging.

For the vast majority of people, Social Security will not even come close to paying for their retirement. And Social Security is known to be insolvent in the near future; means testing — at least — will be required. In other words, most people will not even get the Social Security that they expect. The promises that the government made will not be kept. The Millennials and Gen Z will not be able to pay a phenomenally high Social Security tax to cover the Boomers’ and Gen Xers’ losses.

○ The Americans in question will not retire on capital gains from selling their houses.

If you have $150-250,000 in equity in your house, you may feel rich. However, to get that money, you have to sell your house. But if you sell your house, you have to live somewhere, and rents have been skyrocketing, as have retirement home costs. The money that you get after fees, commissions, and taxes will not last a couple very long. If the couple sells their house when they are 65, and their expenses are just $40,000 a year, in ten years the money they got from selling, their house will be gone. They will be 75 years old, and dead broke.

In other words, most of the Americans who think they can pay for retirement will actually die destitute.

How many Americans are in the age group that may end up in poverty? Over 75 million. Almost a fourth of the U.S. population. And the number in that age group will keep growing.

Between 2009 and 2019, the number of Americans age 45-64 (who will reach age 65 over the next two decades) increased by 4% from 80.3 million to 83.3 million. The number of Americans age 60 and older increased by 34% from 55.7 million to 74.6 million.

“2020 Profile of Older Americans, Administration of Community Living. acl.gov.

Will the Millennials and Gen Z, too many of whom are already financially unstable with less hope for the future than their parents and grandparents had, be able to pay the bills of 75,000,000 impoverished Americans who have lots of needs and are too old to work?

The reality is: If a big crash happens and the government doesn't bail out the markets, then the Boomers and Gen X are likely to die in abject poverty long before their investment portfolios regain their value.

All that has to happen for all this scenario to become real is a big market crash that the government doesn't bail out.

So the government will bail out the stock market again, right? No, probably not. Here's why.

Because the leftists will not be hit as hard by the crash. They have ways to come out way ahead. Think of the situation this way:

The United States owes the Boomers and Gen X a lot of money, the money that older Americans saved and were planning to use to retire. The big crash will simply wipe out that debt. Leaving most of the Boomers and Gen X broke and the U.S. owing them almost nothing. Just a pittance of Social Security, which the Government may find a way not to pay. So the government regulators just got rid of a huge amount of debt.

How the Leftists Get Theirs

Wealth is relative. Even the wealth of some rich leftists would take a hit in a big crash, but most of them have enough money to take losses and retain a good standard of living. Bill Gates, George Soros, and Jeff Bezos don't have anything to worry about, really. Most leftists are well off, especially relative to the working Americans that the leftists’ policies impoverish. And the government leftists will lose little or nothing. Here’s why:

The government-leftists will not lose their savings because the U.S. government will bail out the pensions of the public employees unions, which will lose vast amounts of money in a big stock crash. What will happen is: The government regulators will use taxpayers’ money to cover the losses of the public employees union pension funds after the crash. So the leftists will keep getting pension money, after the people who were productive have lost their savings. In fact, that bailout of union pensions has already started. A 2024 Wall Street Journal article titled “How the Biden-Harris Economy Left Most Americans Behind” reported that when Democrats passed “…$1.9 trillion in new spending... Insolvent union pension funds received a $86 billion rescue.”

Conclusion: Why This is Important!

We said, “…the government has started bailing the market out, making the rich people’s losses good, at the expense of the rest of us.” The U.S. government has become a system for the transfer of wealth from productive Americans to unproductive leftists, who hate America. That is the real reason why the Millennials and Generation Z have failed to enjoy the increase in wealth that previous generations of Americans did. The leftists are stealing it.

The system is rotten to the core. It is essentially an organized crime system. And 99% of the cause is leftist government. To the extent that the Baby Boomers caused this, they are to blame and should be shamed. But the truth is that the growth of a far-left U.S. government dates back at least to the 1930s, and probably further. Sorry Gen X, you now get the short, dirty end of the stick. Thanks to leftists and their overgrown, overbearing leftist government. What are you going to do about it?

Way too much miss understanding of "money" in this post. Please understand we haven't had MONEY in circulation for over 60 years. Here are some clues and I'd highly recommend the reading of https://www.courageouslion.us/p/blood-running-in-the-streets-mobs

"The Federal Government, with the cooperation of the Federal Reserve, has the inherent power to create money--almost any amount of it."

~ The National Debt, Federal Reserve Bank of Philadelphia, p. 8

ALMOST? Why only ALMOST? What keeps them from creating ALL they want? You? Me? Your dog? A full moon?

Federal Reserve Notes are not federal, represent no monetary reserves and no longer conform to the definition of notes. Failing to state who, will pay what, when or to whom - they ceased to be legal tender notes, (offers of money) almost 60 years ago. They are in fact instruments of legalized THEFT.

"...Keynes argues that inflation is a 'method of taxation' which the government uses to 'secure the command over real resources, resources just as real as those obtained by [ordinary] taxation'. 'What is raised by printing notes, ' he writes, is just as much taken from the public as is a beer duty or an income tax.' "

- 1980 Annual Report, Federal Reserve Bank of Richmond, pg 10

"All the paper money issued today is Federal Reserve notes. The real backing for the nation's money is faith in the strength, soundness and stability of the American economy."

~ The Hats the Federal Reserve Wears, Federal Reserve Bank of Philadelphia, pg 4

Faith is what backs our monetary system. YOUR faith. Do you still have faith?

"When plunder has become a way of life for a group of men living together in society, they create for themselves in the course of time a legal system that authorizes it and a moral code that glorifies it."

~ Frederic Bastiat in "The Law"

"Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation,

governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens."

~ 1980 Annual Report, Federal Reserve

Bank of Richmond, pg 6

Isn't confiscation of the wealth of the citizens a nice way of saying STEALING?

"Whenever the legislators endeavor to take away and destroy the property of the people, or to reduce them to slavery under arbitrary power, they put themselves into a state of war with the people, who are thereupon absolved from any further obedience." ~ John Locke (1690)

If the money you earn has no value and you are forced through fiat paper legislation to take it for your labor, are you not having your property (labor) destroyed and are you not being reduced to nothing but slavery? Is not the state at war with the people?

5th Plank Communist Manifesto: Centralization of credit in the hands of the state, by means of a national bank with state capital and an exclusive monopoly.

The Federal Reserve System, created by the Federal Reserve Act of Congress in 1913, is indeed such a “national bank” and it politically manipulates interest rates and holds a monopoly on legal counterfeiting in the United States. This is exactly what Marx had in mind and completely fulfills this plank, another major socialist objective. Yet, most Americans naively believe the U.S. of A. is far from a Marxist or socialist nation.

"The writers of the constitution knew exactly what they were doing when they wrote in Article I Section 10 paragraph 1 'No state shall... make anything but gold and silver coin a tender in payment of debts. ' People able to barter with gold and silver coin control government and are free. Loss of the right to trade in gold and silver coin enslaves people to the creators of psychological 'money.'":

-Merrill Jenkins, Sr.,

Money - The Greatest Hoax on Earth

So you see...they will ALWAYS have enough to keep the slaves enslaved.

Most people worked until they were dead or incapacitated for most of history. I expect same.

I’m 57. So what?

I will object that anyone is taking anyone’s JOB if that job involves working, making, growing, repairing. I don’t know of any productive field or job from service economy, manufacturing, repair, field sales (as opposed to online side gig) agriculture, telecom, merchant marine, military, transoceanic cable repairs, nursing … we have a serious labor shortage. No one wants to work.

The ones that do are in college, overwhelmingly learning weeks of knowledge over a period of years, in exchange for debt slavery and bad habits.

If you mean the email bureaucracy jobs are not hiring… well, learn to work.

LEARN TO WORK. <<